Maritime decarbonisation is the strategic process of reducing and ultimately eliminating greenhouse gas (GHG) emissions from the global shipping industry. Because maritime transport carries around 90% of global trade and accounts for nearly 3% of all anthropogenic GHG emissions, it represents one of the world's most critical “hard-to-abate” sectors. The ultimate goal, mandated by the International Maritime Organization (IMO), is to transition international shipping to net-zero emissions by or around 2050.

Quick Overview: Alternate Fuels for Marine Vessels

- The International Maritime Organization (IMO) has set a net-zero emissions target for international shipping by 2050, with a 20–30% reduction milestone by 2030 — and the countdown has already begun.

- LNG is currently the most commercially mature alternative marine fuel, but methane slip remains a critical unresolved emissions challenge that every fleet operator needs to understand.

- Biofuels offer the fastest path to lower emissions for existing fleets because they work as drop-in solutions with minimal engine modifications — but feedstock availability is a real ceiling on scale.

- Ammonia and hydrogen hold the most promise for true zero-carbon shipping, but technology readiness levels mean neither will be mainstream before 2035 at the earliest.

- One overlooked tool — shore power — can cut port emissions significantly without changing a single thing about your vessel's fuel system, and it's available right now in many major ports.

The shipping industry is responsible for roughly 3% of global greenhouse gas emissions, and that number isn't shrinking fast enough on its own.

It's no longer a future regulatory worry for shipowners, operators, and fleet managers to shift away from heavy fuel oil (HFO). It's a current operational fact. New compliance frameworks, carbon intensity ratings, and fuel availability requirements are reshaping every bunkering decision made today. Sea Transport, a top maritime logistics solutions provider, offers practical guidance for operators navigating this complex transition.

“Maritime Decarbonization | PNNL” from www.pnnl.gov and used with no modifications.

Carbon Emissions in the Shipping Industry: A Larger Issue Than You May Realize

With about 90% of global trade being moved by international shipping, it's not only a vital part of the world economy, but also a significant contributor to emissions. The industry emits approximately 1 billion tonnes of CO₂ equivalent each year. Unlike land-based transportation, there is no simple path to electrification for shipping. The energy density required for long ocean voyages, along with the immense size of global fleets, makes transitioning to cleaner fuels both technically and financially difficult in ways that other industries simply don't experience.

The task is made more difficult by the long lifespan of ships. A ship built today is likely to still be in operation in 2045, long after the IMO's key decarbonisation deadlines. Every decision to build a new ship now either commits to emissions for decades or prepares a fleet for long-term compliance. This is why it is essential for serious maritime operators to understand the full range of alternative fuels – not just those available today, but those that will be commercially viable by 2035 and 2040.

Decarbonization Goals from the IMO That Every Shipowner Should Be Aware Of

In 2023, the International Maritime Organization updated its greenhouse gas strategy, establishing mandatory decarbonization goals that apply to all international shipping. These aren't just wishful thinking — they are the regulations that every future fuel investment decision must be based on. Learn more about the importance of secure liquid fuel storage in a low-emissions future.

2030 Emissions Reduction Target

The IMO has adjusted its strategy to aim for a minimum of a 20% reduction in greenhouse gas emissions from international shipping by 2030, compared to 2008 levels, with a goal of reaching 30%. This target is not as far off as it seems. LNG, in conjunction with operational efficiency measures such as slow steaming, route optimization, and hull fouling management, is the most feasible way to achieve this goal on a large scale. For ships that are already in service, biofuel blends and energy-saving technologies are being implemented as temporary solutions while long-term fuel strategies are being developed.

What Does Net-Zero by 2050 Mean for Fleet Operators?

Net-zero by 2050 means that the entire global fleet must be powered by zero or near-zero carbon fuels in the next 25 years. To put this into perspective, a ship ordered today and delivered in 2027 will still be in service in 2050. This ship needs a credible plan for zero-carbon operation – whether through e-fuels, ammonia, hydrogen, or advanced biofuels – built into its design from the very beginning.

And this is the reason why the idea of “alternative fuel ready” ships is becoming popular. Classification societies like ABS are now helping shipowners to design ships that can adapt to low-flashpoint fuels in the future, including LNG, methanol, ethane, LPG, hydrogen, and ammonia. It's much cheaper to build in that flexibility today than to do a full propulsion conversion in the future.

How CII Ratings and EEXI Are Prompting Immediate Action

Two compliance tools, the Carbon Intensity Indicator (CII) and Energy Efficiency Existing Ship Index (EEXI), are creating a sense of urgency in the short term. CII ratings, which are given a score from A to E, measure a vessel's carbon intensity in actual operation and are recalibrated annually to become stricter over time. A vessel that is rated D or E is subject to increasing corrective action requirements. EEXI, on the other hand, establishes a one-time technical efficiency standard for existing ships. Together, these frameworks are compelling operators to act on fuel efficiency and emissions reduction now, not just in preparation for 2050.

Challenges in Transitioning to Alternative Marine Fuels

While the financial benefits of alternative fuels are becoming more apparent, the process of implementing them is far from simple. The importance of secure liquid fuel storage is a significant factor in ensuring a successful transition to a low-emissions future.

Global Bunkering Networks Infrastructure Gaps

Although LNG bunkering infrastructure has greatly expanded in recent years, it is still concentrated in major hub ports in Europe, East Asia, and North America. LNG availability is inconsistent at best outside these corridors. For methanol, ammonia, and hydrogen, global bunkering infrastructure is still in its early stages. A vessel that runs on green ammonia in Rotterdam may not find a compatible fuel supply in Port Klang or Santos. Until bunkering networks catch up with fuel ambitions, operators of globally trading vessels face a real risk in the supply chain when committing to alternative fuels.

Expensive Vessel Retrofitting and Conversion

Switching an existing ship to operate on LNG, methanol, or ammonia is not a simple upgrade. It needs new fuel tanks (that reduce cargo space), new fuel handling systems, altered or replaced engines, and comprehensive safety system upgrades. For a large container ship, the cost of LNG conversion can reach tens of millions of dollars. For smaller ships, the economics are even more challenging to justify without financial support mechanisms.

Ships that are designed from the beginning to use alternative fuels are significantly more cost-effective over their operational life. This is why the “alternative fuel ready” designation has become a critical factor in ship purchasing decisions. The initial engineering cost to allow for future fuel flexibility is much lower than a conversion after delivery.

“Alternative Fuels in the Maritime …” from www.mdpi.com and used with no modifications.

Training and Certification Requirements for Crew Safety

Each of the alternative fuels—LNG, methanol, ammonia, and hydrogen—possesses unique safety characteristics that necessitate specialized training for the crew. For instance, ammonia is extremely toxic, and exposure to concentrations above 300 ppm can pose immediate threats to life and health. Methanol is not only toxic but also burns invisibly. Therefore, these fuels cannot be safely managed with the conventional training provided for HFO.

Essential Safety Certification Standards for Different Fuel Types

Fuel Type | Main Risk | Necessary Certification Framework |

|---|---|---|

LNG | Cryogenic, flammable | IGF Code, STCW Basic and Advanced Training |

Methanol | Toxic, invisible flame | IGF Code amendments, IMO MSC.1621 guidelines |

Ammonia | Extremely toxic, corrosive | IGC Code, specialized toxicity response training |

Hydrogen | Extremely flammable, low ignition energy | Emerging IGF Code frameworks |

Biofuels (blends) | Similar to VLSFO/MGO | Standard STCW, minimal additional requirements |

The IMO's IGF Code regulates the safe use of low-flashpoint fuels as ship fuel, and it is currently being expanded to include methanol and eventually ammonia. Operators considering a fuel transition need to plan for crew retraining and recertification well in advance of any vessel conversion, rather than as an afterthought.

LNG as Marine Fuel: The Most Developed Alternative On the Market

Liquefied natural gas is the sole alternative marine fuel that is not only commercially available in large quantities but also tested across various ship classes in deep-sea operation. Although it's not the ideal solution, it is the most practical bridge fuel accessible to shipowners who need to address emissions immediately.

The Emission Reductions of LNG vs HFO

When used as a marine fuel, LNG produces around 20-25% less CO₂ per energy unit than HFO. It also nearly eliminates sulfur oxide (SOx) emissions and can reduce nitrogen oxide (NOx) emissions by up to 85% in dual-fuel engines that use the Otto cycle. Emissions of particulate matter are also significantly reduced. These properties have made LNG the preferred fuel for compliance with the IMO 2020 sulfur limits, and they continue to bolster its position as the primary near-term option for decarbonization.

Methane Slip: The Emissions Problem LNG Still Has to Solve

Methane slip refers to the accidental release of unburned methane — the main ingredient of LNG — during the combustion process. This is significant because methane is a powerful greenhouse gas, with a global warming potential approximately 80 times greater than CO₂ over a 20-year timeframe. In low-pressure Otto cycle engines, methane slip can negate a significant portion of the CO₂ reduction benefit that LNG otherwise provides.

High-pressure diesel cycle (HPDF) engines, which are commonly used in many large LNG carriers and newer dual-fuel container ships, are known to produce significantly less methane slip. The technology of these engines is continually improving, and the latest generations of dual-fuel engines have proven to be much more efficient in reducing methane slip compared to those designed just five years ago. However, for fleet operators who are considering the use of LNG, the choice of engine is not a minor decision — it directly affects the actual emissions performance of the fuel.

Overcoming the methane slip issue can be achieved through bio-LNG and e-LNG. Bio-LNG, which is produced from organic waste streams through anaerobic digestion and upgrading, has a nearly zero or even a carbon-negative lifecycle footprint, depending on the feedstock. E-LNG is synthesized using green hydrogen and captured CO₂. Both can be used in existing LNG engines without modification, making them real long-term zero-carbon options for fleets that invest in LNG infrastructure today.

- Otto cycle (low-pressure) engines: Higher methane slip, lower compression, more common in retrofits

- HPDF (high-pressure diesel cycle) engines: Very low methane slip, higher efficiency, preferred for newbuilds

- Bio-LNG: Drop-in compatible with all LNG engines, near-zero lifecycle carbon

- E-LNG: Synthetic, produced from green H₂ and captured CO₂, fully compatible with LNG infrastructure

Choosing the right engine configuration at the newbuild stage is the single most important technical decision for any owner investing in LNG propulsion.

Which Types of Ships Benefit Most From LNG Propulsion

LNG propulsion is most commercially viable for types of ships that operate on fixed routes between ports with established LNG bunkering infrastructure, and that have the hull volume to accommodate LNG tanks without unacceptable cargo capacity loss. Large container ships, cruise vessels, LNG carriers themselves (using boil-off gas), and large bulk carriers operating in the Atlantic and Pacific trade lanes fit this profile well. Smaller coastal vessels and those operating in regions with limited LNG supply infrastructure face a harder economics case — for these, methanol or biofuel blends may present a more practical near-term option.

Methanol: A Carbon-Neutral Contender for Marine Fuel

Methanol is rapidly moving from the sidelines to the mainstream as a marine fuel option. There's a lot to like about methanol. It's a liquid at room temperature, so there's no need for the expensive cryogenic storage that LNG requires. It burns cleaner than HFO, and it already has a global production and distribution network in place. That gives methanol a leg up on ammonia and hydrogen, which don't have the same supply chain advantages.

There is a genuine commercial drive towards methanol. Maersk has pledged to operate a fleet of container ships that can run on methanol. In Europe, a number of ferry operators are already using methanol. The technology is functional, the fuel is accessible, and a regulatory framework for the safe operation of methanol-powered vessels is now established.

Methanol's Global Supply Chain Gives It an Advantage

Methanol is already one of the most widely traded chemical commodities in the world, with approximately 90 million tonnes produced annually. It's stored and transported as a liquid in standard chemical tanker infrastructure, available in ports across Europe, Asia, the Americas, and the Middle East. This existing logistics network dramatically reduces the chicken-and-egg bunkering problem that holds back ammonia and hydrogen. For operators who need a commercially available, lower-carbon alternative fuel today — particularly for vessels operating on routes through established chemical cargo hubs — methanol offers a realistic and scalable option that no other zero-carbon candidate can currently match.

Rules for Methanol-Fueled Ships: IMO MSC.1621

The interim guidelines for ships that use methanol as fuel are provided by IMO circular MSC.1/Circ.1621. These guidelines cover everything from where to place fuel tanks to ventilation requirements, firefighting systems, and safety protocols for crew members. Methanol has a low flashpoint of 11°C, which means it falls under the low-flashpoint fuel provisions of the IGF Code. This requires a dedicated design for safety systems. If an operator is planning a newbuild or conversion that is fueled by methanol, they must design to these guidelines from the beginning. Retrofitting safety systems that weren't designed in from the start is significantly more expensive and technically constrained.

Why the Source of Methanol is Important: Green vs. Grey Methanol

Not all methanol is created equal when it comes to reducing carbon emissions. Most of the methanol produced today is grey methanol, which is made from natural gas through a process called steam methane reforming. This type of methanol has a carbon footprint that is only slightly better than traditional marine fuels over their entire lifecycle. While using grey methanol does reduce SOx and particulate matter emissions, it doesn't do much to reduce greenhouse gas emissions. For a more sustainable approach, exploring the circular economy could provide better alternatives.

On the other hand, green methanol is produced either from biomass (bio-methanol) or from green hydrogen combined with captured CO₂ (e-methanol). Bio-methanol can achieve lifecycle carbon reductions of up to 65–95% compared to HFO, depending on the feedstock. E-methanol, when produced using renewable electricity, is effectively carbon-neutral. The challenge is supply — green methanol currently represents a small fraction of global methanol production. Maersk and other early adopters are actively contracting green methanol supply to support their dual-fuel methanol fleet investments, which is beginning to stimulate production scale-up. For operators investing in methanol-capable vessels today, the expectation is that green methanol supply will grow substantially through the 2030s.

Biofuels: An Instant Fix for Current Fleets

For those who currently manage a fleet and need to cut emissions without waiting for new builds or costly conversions, biofuels are the most readily usable option. They are compatible with existing engines, increasingly available from a growing number of refueling stations, and require little to no changes to current fuel systems.

Which Biofuel Mixtures Can Be Used in Current Marine Engines

Marine biofuels are usually mixed with traditional fuels, most often VLSFO or MGO. B20 mixtures — 20% biofuel, 80% traditional fuel — are generally accepted as the highest ratio that can be used without modifying the engine in most current marine diesel engines, though some engine manufacturers have approved higher mixture ratios. The most common marine biofuel sources include used cooking oil (UCO), palm oil methyl ester (POME), and various animal fats processed into FAME (fatty acid methyl esters) or hydrotreated vegetable oil (HVO).

Hydrotreated vegetable oil (HVO), also known as renewable diesel, is especially suitable for marine applications due to its close chemical resemblance to conventional diesel. It has superior cold flow properties compared to Fatty Acid Methyl Ester (FAME) blends and is more stable when stored. Many leading bunker suppliers now provide HVO-based marine biofuel blends in major European and Asian ports. As demand increases, the number of locations where it is available is also growing.

Feedstock Quality and Availability: The Limiting Factor for Biofuels

The most significant limitation on the viability of biofuels as a long-term solution for marine decarbonization is feedstock. Sustainable feedstocks — waste oils, agricultural residues, non-food biomass — are finite. As demand from aviation, road transport, and shipping all compete for the same waste oil streams, prices rise and supply tightens. The International Maritime Organization and major certification bodies including ISCC (International Sustainability and Carbon Certification) have developed sustainability frameworks to ensure biofuels used in shipping are genuinely low-carbon and not driving deforestation or land-use conflicts. Operators sourcing marine biofuels must verify sustainability certification rigorously, not just for ethical reasons, but because regulators and carbon accounting frameworks require it.

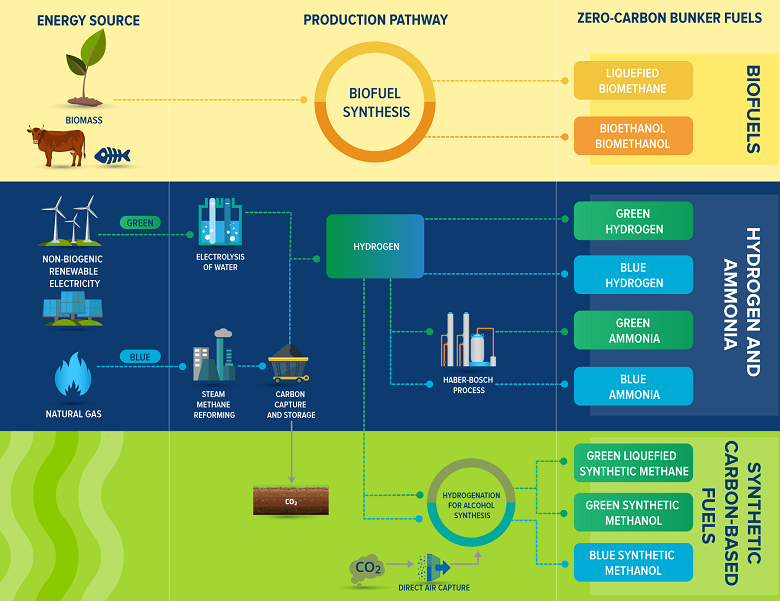

Ammonia and Hydrogen: The Future's Zero-Carbon Fuels

Ammonia and hydrogen could be the ultimate solution to marine decarbonization. These fuels, when produced from renewable energy, contain no carbon at all. The journey to achieve this involves overcoming technical, safety, and infrastructure hurdles that are considerable but not impossible. The timeline for mainstream commercial use of both fuels is mainly between 2035 and 2045. However, the investment decisions that will decide whether this timeline is achievable are being made at this very moment.

Why Ammonia Is Toxic but Still a Leading Decarbonization Candidate

Ammonia is a zero-carbon fuel. When it's used in a fuel cell or burned, the only byproducts are nitrogen and water vapor. This makes it one of the best energy carriers that can be stored and transported as a liquid when it comes to zero-carbon credentials. However, it's not perfect. Ammonia is highly toxic, even at low concentrations, and it can corrode certain materials. It also has a narrow flammability range, which complicates the design of combustion engines. On top of that, burning ammonia produces nitrogen oxide (NOx) emissions, which is a problem that engine developers are trying to solve.

Despite these challenges, ammonia's energy density per volume, which is significantly higher than compressed hydrogen, and its established global production and transport infrastructure, which primarily serves the fertilizer industry, make it the top candidate for zero-carbon fuel in large, long-haul vessels. Both MAN Energy Solutions and WinGD have announced designs for ammonia-capable two-stroke engines, aiming for commercial availability in the mid-2020s. For a deeper understanding of the sustainability conversation surrounding long-distance transport, further reading is available.

Addressing the Energy Density Problem of Green Hydrogen

Hydrogen has the highest energy content per unit of mass of any fuel. It has about three times the energy content of diesel by weight. The problem is by volume. Compressed hydrogen at 700 bar holds much less energy per cubic meter than LNG or methanol. Liquefied hydrogen requires storage at -253°C, which is even colder than LNG. This makes the complexity and cost of the cryogenic system a significant barrier.

Hydrogen is best suited for use in fuel cells for smaller marine vessels such as ferries, harbor craft, and short-sea shipping. This is due to the fact that the efficiency benefits of fuel cell propulsion can compensate for the volumetric storage penalty. There are already hydrogen fuel cell ferries operating in Norway and California, proving that it is technically feasible on a smaller scale. Hydrogen's storage challenges make it less practical than ammonia as a direct fuel for deep-sea shipping. However, it is still crucial as a raw material for the production of green methanol and e-ammonia.

Preparedness of Ammonia and Hydrogen Marine Engines

The readiness of ammonia and hydrogen marine propulsion technology varies greatly depending on the application. Hydrogen fuel cell systems for smaller vessels are at TRL 7–8, meaning they've been demonstrated in operational environments and are commercially available. Large two-stroke ammonia combustion engines, on the other hand, are at TRL 4–6, indicating that they've been demonstrated at the component or prototype level but are not yet in commercial fleet service. The gap between technology that has been proven in a laboratory and a certified engine that is available for newbuild orders is real, but it is closing faster than many expected five years ago.

Organizations such as ABS, DNV, and Lloyd's Register are currently working on establishing regulations for ammonia and hydrogen fuels. There are also a number of pilot projects planned for ammonia-fueled ships, which are expected to start sea trials between 2024 and 2026. Those who are currently ordering new ships to be delivered between 2027 and 2029 should pay close attention to the results of these trials. The results will likely have a significant impact on the commercial availability and insurance options for ammonia propulsion in the early 2030s.

Shore Power: The Underestimated Decarbonization Solution Already in Your Harbor

As the industry discusses which alternative fuel will be the most used by 2040, there is a zero-emission solution available right now in many major harbors that requires no fuel change at all: shore power, also known as cold ironing or alternative maritime power (AMP). When a vessel connects to the onshore power grid while docked, it completely shuts down its auxiliary engines — eliminating all fuel combustion and related emissions during harbor stays.

Studies suggest that the adoption of shore power could reduce the proportion of non-compliant vessels from 47.4% to 40% by 2040, a significant short-term compliance advantage that is much less expensive than converting the fuel system. The FuelEU Maritime regulation of the EU, which took effect in 2024, requires container ships and passenger vessels to connect to shore power at EU ports starting in 2030, indicating that this is not a voluntary measure but a future compliance obligation.

How Shore Power Connections Can Reduce Port Emissions Without Changing Fuel

The reduction of emissions from shore power is dependent on the carbon intensity of the local electricity grid. In countries where there is a high penetration of renewable energy, such as Norway, Denmark, and parts of the US Pacific Coast, shore power can provide near-zero operational emissions during port calls. In regions where the grid is heavily reliant on coal, the benefit is reduced, but it is still significant for local air quality, as it eliminates SOx, NOx, and particulate emissions directly in port communities. As electricity grids decarbonize globally throughout the 2030s, the emissions benefit of shore power will increase automatically, without the need for any further action by the vessel operator.

Shore Power Could Lower Non-Compliant Vessels From 47.4% to 40% by 2040

Shore power may not be the ultimate solution, but the numbers are persuasive. Projections suggest that if shore power is adopted widely at major global ports, the percentage of non-compliant vessels could drop from 47.4% to 40% by 2040 — without needing to modify a single engine or alter any fuel systems. For fleet operators who need to manage compliance risk across a fleet of various ages, this is a significant reduction that could be achieved for much less than the cost of converting a vessel. For more information on alternative fuel options, visit this resource.

Selecting the Appropriate Alternative Fuel for Your Ship

There isn't a one-size-fits-all solution — and anyone who tells you there is isn't considering the full complexity of your operational circumstances. The best alternative fuel for you will depend on the type of ship you have, your trading routes, the age of your fleet, your capital position, and how you balance short-term compliance risk with long-term fuel transition exposure.

What is clear from the evidence is this: the highest-risk strategy now is to do nothing. CII ratings are getting stricter every year. Carbon taxes are on the rise. There's no guarantee that HFO fuel will be available in all ports after 2030. The question is no longer whether to make the transition, but rather which fuel to choose, how quickly to do it, and in what order.

Choosing the Right Fuel for the Job

- Deep-sea container ships and bulk carriers on fixed routes between LNG-capable hub ports: LNG dual-fuel newbuilds with HPDF engines, with a transition pathway to bio-LNG and e-LNG through the 2030s.

- Cruise ships and large ferries with predictable port schedules: Methanol dual-fuel or LNG, combined with mandatory shore power connectivity at home ports.

- Short-sea and coastal operators with existing vessels: Biofuel blends (B20 HVO) as an immediate emissions reduction tool while evaluating methanol or ammonia for next vessel order.

- Harbor craft, tugs, and passenger ferries on fixed short routes: Hydrogen fuel cell propulsion or battery-electric with shore charging — the energy density constraints that make hydrogen impractical for ocean-going vessels are irrelevant at this scale.

- Vessels trading in EU waters with regular port calls: Shore power connectivity is a compliance imperative from 2030; plan for it in any current refurbishment or newbuild specification.

The length of a route is likely the most significant factor in fuel selection. Short, predictable routes allow for smaller fuel tank volumes and access to fixed bunkering points — which makes hydrogen, battery-electric, and methanol practical options. Long ocean voyages require energy-dense fuels with global bunkering availability, which currently means LNG or biofuel blends for existing vessels and LNG or methanol for newbuilds.

It's also important to consider the size of the vessel. The large two-stroke slow-speed engines that are typically used in VLCCs, large bulk carriers, and ultra-large container ships have different alternative fuel compatibility profiles than the medium-speed four-stroke engines used in smaller vessels. If you're making a fuel strategy decision for newbuilds, you should review the MAN and WinGD engine roadmaps for LNG, methanol, and ammonia compatibility.

Why Short-Term and Long-Term Fuel Strategies Need Different Plans

Short-term strategies, which cover the next five years, are mainly about complying with regulations. This involves using biofuel blends, making operational efficiency improvements, and using shore power to manage CII ratings and EEXI compliance. At the same time, companies need to avoid the risk of stranded assets that could result from over-committing to a single fuel pathway before the technology landscape becomes clearer. Long-term strategies, which look ahead to 2030 to 2050, are about deciding which zero-carbon fuel infrastructure to invest in. These two planning horizons need completely different frameworks, stakeholders, and financial models. Mixing them up is one of the most frequent and expensive errors in fleet decarbonization planning.

Financial Incentives and Their Impact on the Business Case for Alternative Fuels

While the economics of alternative marine fuels are becoming more favorable, they are not yet on par with HFO or VLSFO without policy support. Green methanol is currently priced significantly higher than conventional marine fuels. The cost advantage of LNG over HFO varies with natural gas market prices. Biofuels are more expensive than conventional fuels in most markets. Financial incentives — such as carbon pricing mechanisms, fuel subsidies, green shipping corridors, and preferential port dues — are key factors in the business case for any alternative fuel investment.

The European Union Emissions Trading System (EU ETS) has now been extended to include maritime shipping. Starting in 2024, shipping companies will have to surrender carbon allowances for 40% of emissions from voyages within the EU. This will increase to 70% in 2025 and 100% in 2026. This places a direct financial cost on the use of Heavy Fuel Oil (HFO), making Liquefied Natural Gas (LNG), methanol, and biofuels more economically attractive for vessels operating in European waters. The FuelEU Maritime regulation will introduce a target for the greenhouse gas intensity of energy used on board vessels trading in the EU from 2025.

Green shipping corridors, which are agreements between two port authorities to create zero-emission shipping lanes, often come with benefits such as reduced port fees, priority access to berths, and joint investment in bunkering infrastructure. If a ship operator's routes align with an existing or emerging green corridor, they can access financial incentives that significantly shorten the payback period for investments in alternative fuels. The Clydebank Declaration, which was signed by 22 countries at COP26, pledged to establish a minimum of six green shipping corridors by the mid-2020s. For more on sustainability in long-distance transport, see this conversation on sustainability.

Utilizing Simulation Tools to Determine Fuel Needs and Emissions Prior to Making a Commitment

Prior to investing in a fuel system conversion or newbuild specification, it is crucial to carry out quantitative modelling of actual propulsion demand under real operating conditions. The tools for carrying out this process, both academic and commercial, are now highly developed and readily available. Research in this area has made use of MATLAB/Python algorithms which retrieve real-time vessel position data in order to simulate propulsion demand profiles across actual routes. This provides a far more accurate image of fuel consumption and emissions performance than simply relying on nameplate engine specifications.

What these simulations consistently show is that the variability of the operational profile — weather routing, port waiting times, laden versus ballast passages — creates a significant gap between theoretical fuel performance and actual results. A fuel that seems ideal on paper for a specific trade route may not perform as well when actual voyage data is taken into account. This is especially relevant for LNG, where engine loading profiles affect methane slip, and for methanol, where energy density differences compared to HFO affect range calculations.

Before deciding on a fuel transition, you should consider the following factors:

- The actual propulsion demand profile over a 12-month voyage dataset, not just the theoretical design speed

- The volume requirements for fuel tanks and their impact on cargo carrying capacity and stability

- The frequency of bunkering requirements along the actual trading routes

- The lifecycle carbon intensity of the specific fuel supply chain being considered, not just generic averages

- The trajectory of the CII rating under the new fuel regime over the remaining operational life of the vessel

Several classification societies offer their own fleet decarbonization modelling tools. These include ABS's My Digital Fleet platform, DNV's Veracity ecosystem, and Lloyd's Register's fuel transition advisory services. All of these services incorporate voyage data analysis into their assessments. It is worth investing in these services before finalizing a fuel strategy. The cost of a thorough fuel feasibility study is negligible compared to the cost of a wrong capital commitment on a vessel with a 25-year operating life.

By 2040, E-Fuels Will Be the Mainstay of Marine Shipping — Here's What Needs to Be Done Now

The future is certain: e-fuels — e-methanol, e-ammonia, e-LNG, and eventually green hydrogen — will be the primary zero-carbon energy sources for deep-sea shipping as the cost of renewable electricity continues to decrease and the production of green hydrogen expands throughout the 2030s. The International Energy Agency and numerous maritime decarbonization research organizations have developed scenarios in which e-fuels provide the majority of marine fuel energy by 2050. The competition is not about whether e-fuels will be the mainstay, but about which e-fuel will be the most successful in which vessel segment — and whether your fleet is ready to take advantage of the transition rather than being left behind. The necessary action is not to wait for the best fuel to be identified, but to incorporate fuel flexibility into every new build and major conversion decision, invest in crew skills for low-flashpoint fuels, and participate in the development of green corridors and port infrastructure that will determine where zero-carbon bunkering is first available.

Common Questions

These are the questions most often asked by operators when they start planning their transition to alternative fuels.

Which alternative fuel is the most feasible for marine vessels at present?

Fuel

Commercial Maturity

Carbon Reduction vs HFO

Best Application

LNG

High — widely available

20–25% CO₂ reduction (combustion)

Large deep-sea vessels on hub routes

Biofuels (HVO/FAME blends)

High — drop-in compatible

Up to 65–90% lifecycle reduction

Existing fleet, immediate compliance

Methanol

Medium-High — growing fast

Up to 95% (green methanol)

Container ships, ferries, chemical tankers

Ammonia

Low-Medium — pre-commercial

100% (green ammonia)

Future deep-sea, large bulk

Hydrogen

Low — emerging

100% (green hydrogen)

Short-sea, harbor craft, fuel cells

At the moment, LNG is the most commercially feasible alternative fuel for deep-sea shipping. It has tested engine technology, a growing global bunkering network, and a proven reduction in emissions compared to HFO. For existing fleets that cannot justify a full conversion, biofuel blends — particularly those based on HVO — are the most immediately implementable option. They require no modifications to the engine and provide significant lifecycle carbon reductions when certified sustainable feedstocks are used.

As of 2024, methanol is the most rapidly expanding alternative fuel in newbuild orders. This growth is fueled by its ability to be stored at room temperature, its well-established supply chain, and the viable pathway to green methanol that will be available through the 2030s. For those placing newbuild orders today, methanol dual-fuel is becoming a more competitive choice compared to LNG dual-fuel.

But the truth is, the choice of fuel depends on the type of vessel and its route. A fuel that works best for a container ship crossing the Pacific may not be the best choice for a supply vessel in the North Sea or a ferry in the Adriatic. Making the right choice requires modeling operational data, not following generic industry advice.

How much do financial incentives reduce the cost of switching to alternative marine fuels?

The quantitative impact of financial incentives varies significantly by jurisdiction and incentive type. The EU ETS carbon cost creates a direct financial penalty for HFO use that is currently equivalent to tens of dollars per tonne of CO₂ — a cost that will rise as the carbon price increases and the free allowance phase-out completes by 2026. Modelling by multiple maritime economics bodies suggests that at EU ETS carbon prices above approximately €80–100 per tonne CO₂, LNG and methanol become cost-competitive with VLSFO on a total cost of ownership basis for EU-trading vessels. Green corridor participation and port incentive programs can further shift the economics, though these vary too widely by location to generalize into a single figure.

Will ships still use HFO after 2040?

It's highly likely — but its role will be much smaller, it will be subject to a significant carbon cost, and it will only be used where there is no viable alternative. The IMO's decarbonization trajectory does not explicitly ban HFO, but the combination of carbon pricing under the IMO's market-based measure framework (expected after 2027), CII rating requirements that tighten every year, and FuelEU Maritime's greenhouse gas intensity targets will make HFO increasingly expensive and operationally constraining. By 2040, ships still running on HFO will face high carbon levy costs, limited access to EU ports, and potential difficulty obtaining competitive freight rates from charterers with their own Scope 3 emissions commitments.

Heavy Fuel Oil (HFO) will continue to be used in certain trades, especially those outside the EU and IMO convention countries, and for types of vessels not covered by the major regulatory frameworks, even after 2040. However, for any ship operating in regulated markets or serving major global shippers with net-zero supply chain commitments, the use of HFO post-2035 poses a significant and growing business risk.

How are bio-LNG and e-LNG different?

Bio-LNG and e-LNG can both be used in existing LNG engines and infrastructure without any changes — this means that any ship that's already equipped for LNG propulsion can use them. The only difference is how they're made, which affects their carbon footprint and how much they can be scaled up in the long term. For more on sustainability in transportation, check out this sustainability conversation on long-distance transport.

- Bio-LNG: Bio-LNG is created from organic waste streams, such as agricultural residues, food waste, sewage sludge, and other biomass feedstocks. It is produced through anaerobic digestion, followed by upgrading and liquefaction. Depending on the feedstock, it can achieve near-zero or even carbon-negative lifecycle emissions. However, the supply is limited by the available sustainable biomass.

- E-LNG (synthetic LNG): E-LNG is produced by combining green hydrogen, which comes from renewable-powered electrolysis, with captured CO₂ via methanation. The resulting synthetic methane is then liquefied. It is completely carbon-neutral when renewable electricity is used. It is scalable with the expansion of renewable energy but is currently very expensive to produce.

Bio-LNG is nearer to being commercially available at scale in the near term. There are several European production facilities already operational or under construction. E-LNG is a longer-term proposition. Its cost will decrease as green hydrogen production scales and electrolyzer costs decrease through the 2030s.

For those who are currently investing in LNG infrastructure, the most important thing to remember is that the same tanks, engines, and bunkering connections that currently use fossil LNG can also use bio-LNG or e-LNG in the future. The investment in infrastructure does not become obsolete with the transition to cleaner energy — instead, it becomes the delivery method for zero-carbon fuel as the supply increases.

What role does shore power play in maritime decarbonization efforts?

Shore power completely removes all emissions from auxiliary engines during port calls by plugging the ship into the onshore grid. For ships that spend a lot of time docked — such as cruise ships, ferries, and container ships at major transhipment hubs — emissions during port calls make up a significant portion of total operational emissions. Shore power can completely eliminate these emissions, making it one of the most impactful and cost-effective actions available for short-sea and port-intensive trades.

Decentralized Renewable Energy Decarbonisation Solutions & Innovations

Decentralized renewable energy is transforming power generation by producing electricity where it’s needed, challenging the age-old centralized grid. Technologies like rooftop solar, battery storage, and green hydrogen drive this shift, presenting solutions to energy accessibility and decarbonization challenges across the globe, particularly in underserved regions like Sub-Saharan Africa…

Decentralized Renewable Energy Decarbonisation Solutions & Innovations

Decentralized renewable energy (DRE) is changing the energy landscape by generating power near the point of use, enhancing efficiency and equity. This local approach empowers communities while tackling energy access and decarbonization, making it a critical solution for a sustainable future…

Climate Change Risk Management Strategies & Solutions

Climate change risk management is essential now. Combining mitigation, adaptation, geoengineering, and expanding knowledge offers the best approach. Effective partnerships between scientists and field specialists drive real-world climate solutions. Discover strategies to reduce vulnerability across forests, water systems, and wildlife habitats for a sustainable future…

The Future of Sustainable Bio-based Materials and Products

Bio-based materials are products and materials made from renewable biological resources like plants, animals, and microorganisms. They are a sustainable alternative to traditional fossil-fuel-based products, offering advantages such as a smaller carbon footprint and reduced reliance on finite resources. Common examples include timber, hemp, and bio-based plastics like polylactic acid (PLA), and they are used […]